Our last Macro newsletter focused on consumer sentiment, rising treasury yields and housing data. This week’s newsletter discusses the looming stimulus bill, unemployment numbers and U.S. mobility.

Subscribe now to never miss an update:

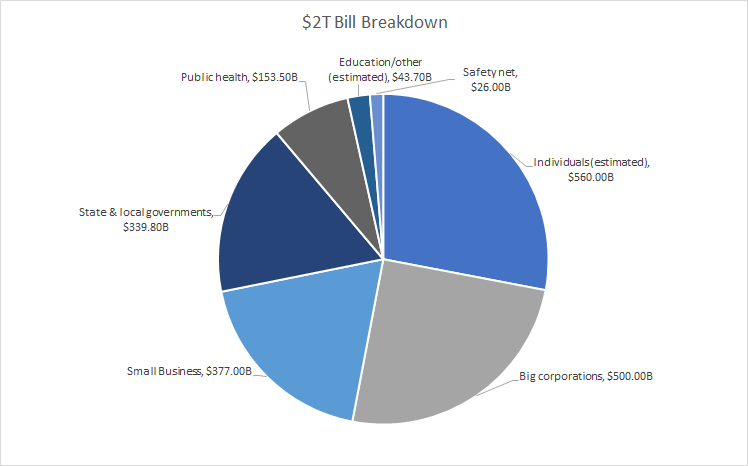

Biden’s Stimulus Bill:

Source: National Public Radio, chart created by The Macro Mail

The $1.9 trillion stimulus bill passed the senate on Saturday and is set to be voted on by the House today. Here are the highlights for what the bill includes:

Direct $1,400 payments to individuals earning less than $75,000 or couples earning less than $150,000 plus $1,400 per dependent

Weekly unemployment benefits extended through September 6th

Funding for food security programs including $8.8 billion for student meals

Loan and interest payments on student loans deferred through September 30th with no penalty to borrower for all federally owned student loans

Emergency grants and forgivable loans for small businesses (500 or fewer employees)

$500 billion in loans and other programs for big corporations including ~$58 billion for airlines

$100 billion for hospitals responding to COVID-19

$340 billion for state and local government programs

The bond market is betting on inflation arising as a result of the bill, with 10-year treasury yields hovering above 1.6% and the 5-year forward inflation expectation rate now above 2%.

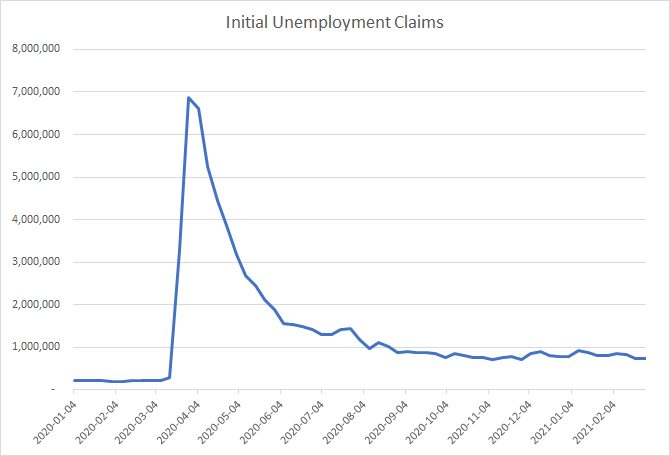

Employment:

Weekly initial unemployment claims is a leading economic indicator put together by the Department of Labor tracking the number of initial claims for unemployment insurance filed by individuals after separation from an employer. Initial claims recently hit their lowest level since November, with hiring spurred on by stimulus and reopening optimism.

Source: Federal Reserve Economic Data, chart created by The Macro Mail

Coinciding with this data, the U.S. economy added 379,000 new jobs in February, with the national unemployment rate falling from 6.3% in January to 6.2% despite labor force participation increasing. The biggest sectors contributing to jobs growth were Leisure & Hospitality and Temporary Help.

Goldman Sachs economists are anticipating a hiring boom later this year, fueled by economic reopening, Biden’s stimulus package and pent-up savings. The bank is forecasting the unemployment rate to drop to just 4.1% by the end of the year, but this could be even lower if the stimulus package and vaccines have a greater impact than initially anticipated.

U.S. Mobility and COVID-19:

Google’s mobility reports provide a keen insight into how consumers are acting under COVID-19 lockdown measures. The data shows mobility trends in the following areas:

Retail and Recreation

Grocery and Pharmacy

Parks

Transit Stations

Workplaces

Residential

The data is presented as an index, with a baseline derived from average mobility for that day of the week from the 5‑week period between January 3rd and February 6th, 2020.

Source: Google Community Mobility Reports, chart created by The Macro Mail

After registering a steady decline since October 2020, U.S mobility has jumped across the board, with vaccines rolling out and COVID-19 cases and deaths registering steep declines. This is good news for business, especially leisure and hospitality which has been hit hardest by the pandemic. However, according to the University of Washington, one of the factors that could pose a threat to this improvement is the spread of the UK’s B.1.1.7 variant of the virus, which could become a dominant strain in the U.S. by spring. The other factor is behaviors. Improvements in infection rates were aided by increased mask-wearing and decreasing mobility over the winter. Going forward, it’s critical that people adhere to social distancing measures and the vaccine rollout ramps up.

Disclaimer: All material presented in this newsletter is not to be regarded as investment advice, but for general informational purposes only. You are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. By reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer.