Weekly Macro Update: Economic Picture Remains Mixed

Weekly Macro Update: Economic Picture Remains Mixed

Last week’s newsletter focused on the ISM Services Index. This week’s newsletter provides a general update on the U.S. macroeconomic picture. Here are the highlights:

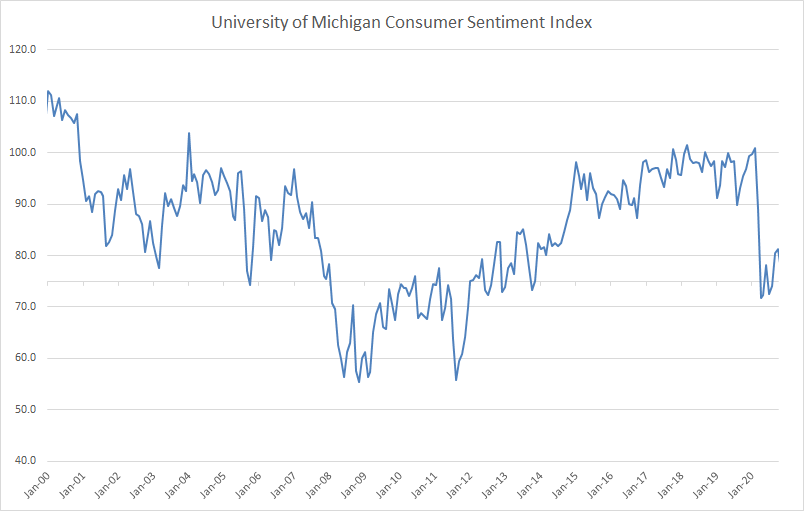

Despite a dip in November, consumer sentiment towards current economic conditions and future expectations is up in December.

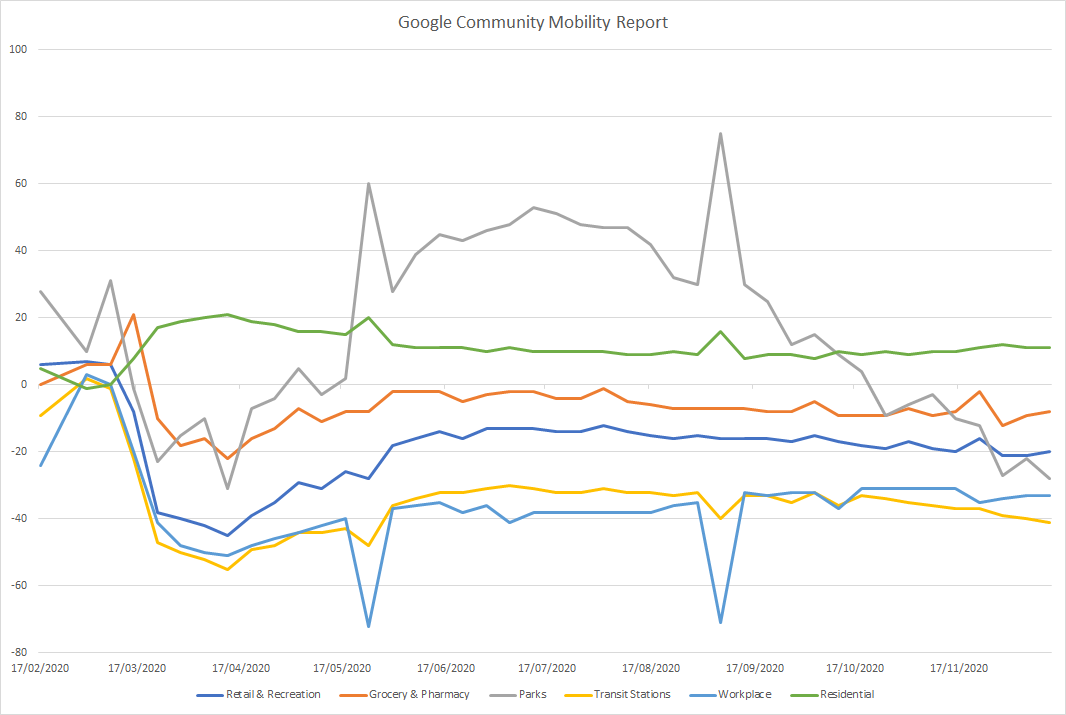

Mobility in retail & recreational spaces and grocery & pharmacy stores has been steadily declining since September.

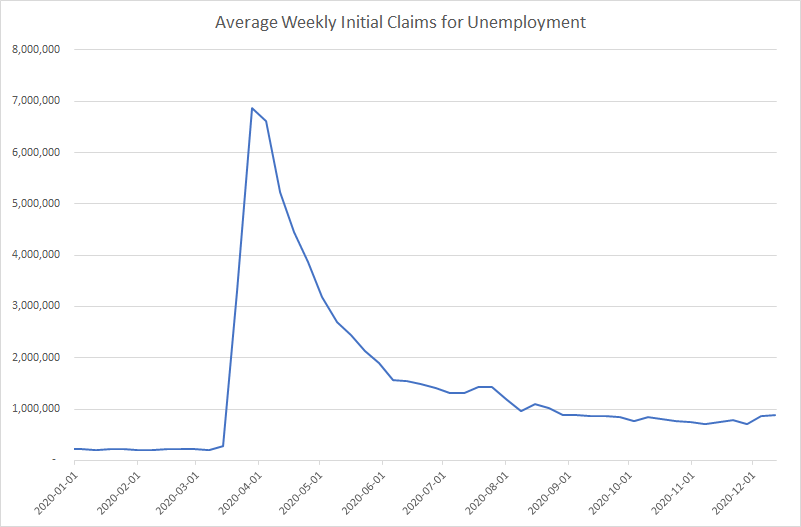

Initial unemployment claims appear to have plateaued and may be on the rise.

Building permits and housing starts data remains solid, fueled by record-low interest rates.

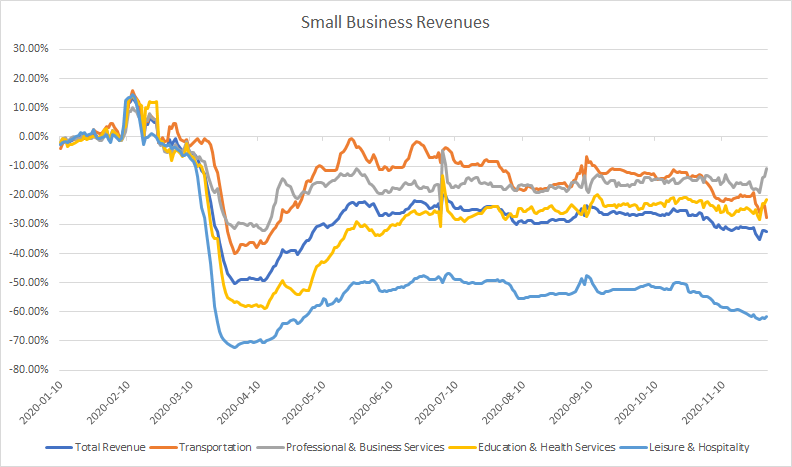

Small business revenues remain 32% below pre-COVID levels with leisure & hospitality declining at a faster pace.

Consumer Sentiment:

Source: University of Michigan, chart created by The Macro Mail

Consumer sentiment is an important leading macroeconomic indicator. Consumer sentiment drives the consumption of consumer discretionary goods, which typically carry a higher profit margin, driving net earnings. As such, the University of Michigan Consumer Sentiment Index is a useful leading indicator of corporate performance.

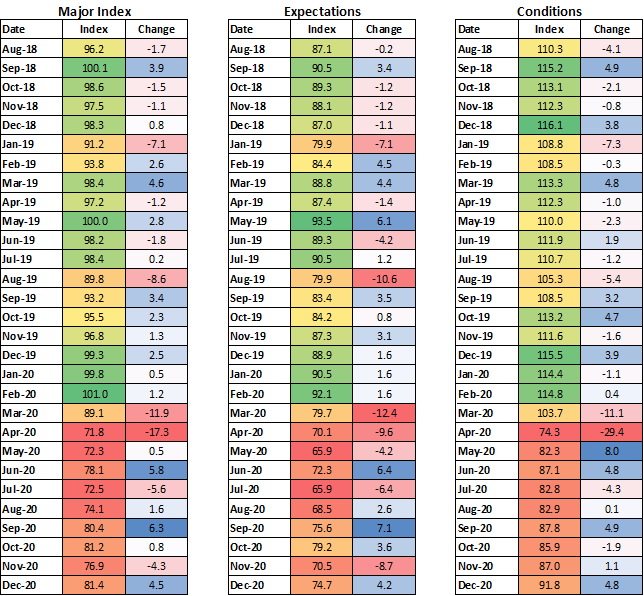

Preliminary results for December show a surprising increase in sentiment, with the current conditions index up by 4.8 points and the consumer expectations index up by 4.2 points.

Source: University of Michigan, table created by The Macro Mail

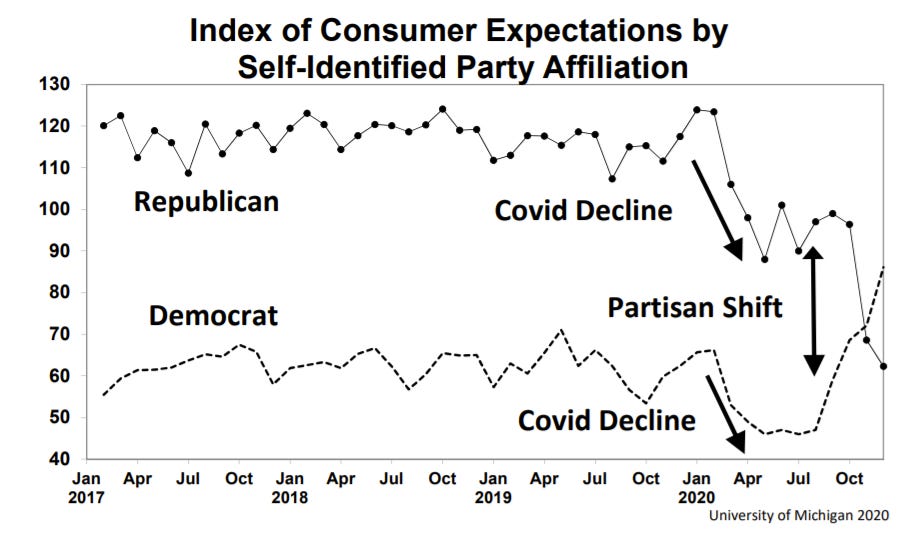

The early December gain in consumer sentiment was largely the result of an improving economic outlook spurred on by encouraging vaccine news, despite a rising number of COVID-19 cases and deaths. Political trends have also contributed. Between August and December the consumer expectations index among self-identified Democrats rose by 39.5 points, but fell by 34.9 points among self-identified Republicans, largely due to the election victory of Joe Biden.

With further shutdowns imminent, it is likely that job losses and income declines will continue to persist in the short run; however, the data paints a positive picture for longer-term consumer spending recovery.

Source: University of Michigan

Google Mobility Data:

Google’s mobility reports provide a keen insight into how consumers are acting under COVID-19 lockdown measures. The data shows mobility trends in the following areas:

Retail and Recreation

Grocery and Pharmacy

Parks

Transit Stations

Workplaces

Residential

The data is presented as an index, with a baseline derived from average mobility for that day of the week from the 5‑week period between January 3rd and February 6th, 2020.

Source: Google Community Mobility Reports, chart created by The Macro Mail

Since July, mobility in retail & recreational spaces has steadily declined as a new wave of COVID-19 cases and subsequent lockdowns have stifled mobility. The same is true for grocery & pharmacy stores. The new Coronavirus variant which plunged parts of the UK back into full lockdown will likely put further pressure on U.S. officials to take similar measures. It is therefore likely that mobility in these spaces will continue to decline, and sectors which are particularly sensitive to mobility, such as hospitality, will continue to suffer.

Employment:

Weekly initial unemployment claims is a leading economic indicator put together by the Department of Labor tracking the number of initial claims for unemployment insurance filed by individuals after separation from an employer. Despite early improvements on this front, initial claims have remained flat since September and appear to be picking up, with a 20.4% increase in unemployment claims for the week ending 12/06. Should further lockdown restrictions be implemented it is likely that this will continue to rise.

Source: Federal Reserve Economic Data, chart created by The Macro Mail

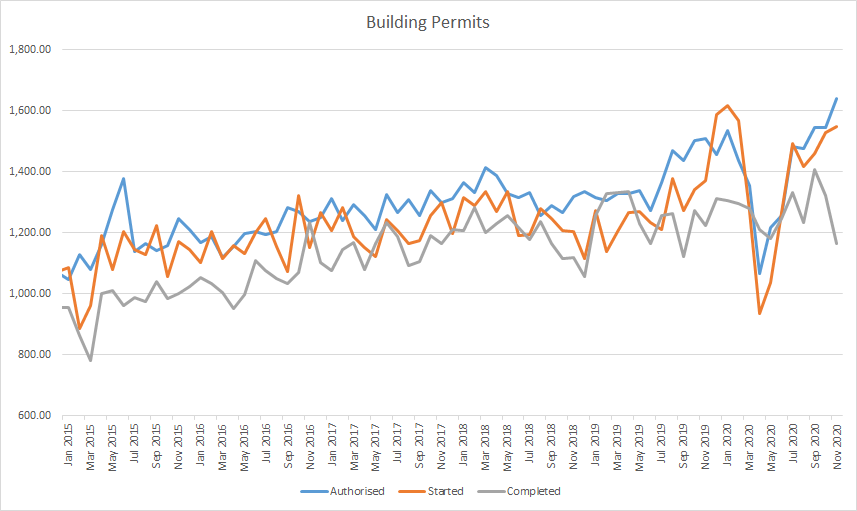

Housing:

The U.S. Census Bureau and the U.S. Department of Housing and Urban Development jointly release seasonally adjusted housing statistics every month. These statistics are important because the housing market is a good indicator of overall economic health.

Authorized building permits for November were up 6.2% from the revised October rate and 8.5% above the November 2019 rate. Housing starts grew by 1.2% since October and 12.8% since November 2019. Housing completions, however, were 12.1% below the revised October rate and 4.9% below the November 2019 rate.

Authorized permits tend to lead housing starts and completions. With permits and housing starts continuing to grow, it is likely that the run-up in housing demand, propped up by record-low interest rates, is set to continue.

Source: United States Census Bureau, chart created by The Macro Mail

Small Business Revenues

Analyzing small business revenues is one of the most effective ways to gauge overall U.S. economic recovery. According to Womply data shown on Track The Recovery, small business revenues remain 32% below pre-COVID levels, with Professional & Business Services and Transportation outperforming other small businesses. Leisure & Hospitality revenues continue to lag behind, down 62%, as this sector is particularly sensitive to rising COVID-19 cases and lockdown measures. This trend will likely continue as the new strain of Coronavirus puts further pressure on hospitality businesses to close operations. The full Opportunity Insights paper covering this data can be read here.

Source: Track The Recovery, chart created by The Macro Mail

Key Quotes:

“The global economic recovery will strengthen and become more sure-footed from the middle of next year as coronavirus vaccines are rolled out and social distancing starts to unwind” - Fitch Ratings

“We look for a rocky start to the new year as many countries battle Covid outbreaks. However, a combination of fiscal stimulus and wide vaccine distribution should boost growth by mid-year [2021]. Despite the recovery, global inflation likely will remain low and many policy rates likely will remain stuck near zero.” - Bank of America Global Research

"The package is more anti-depressant than stimulus, although sending adult Americans $600 might lead to more spending." - UBS Global Wealth Management

“Pro-cyclical assets remain well-positioned heading into 2021, and we expect higher equity and commodity prices, tighter credit spreads, steeper rates curves and a weaker Dollar.” - Goldman Sachs Global Macro Research

Was this email forwarded to you? Subscribe here.

Follow us on twitter to never miss a post.